Written by: Sunny, Messari Research

Translated by: Alex Liu, Foresight News

In the past few years, traditional finance (TradFi) has gradually lost its source of growth narrative. Artificial intelligence has been over-allocated, and software companies no longer have the imaginative space they had in the 2000s and 2010s.

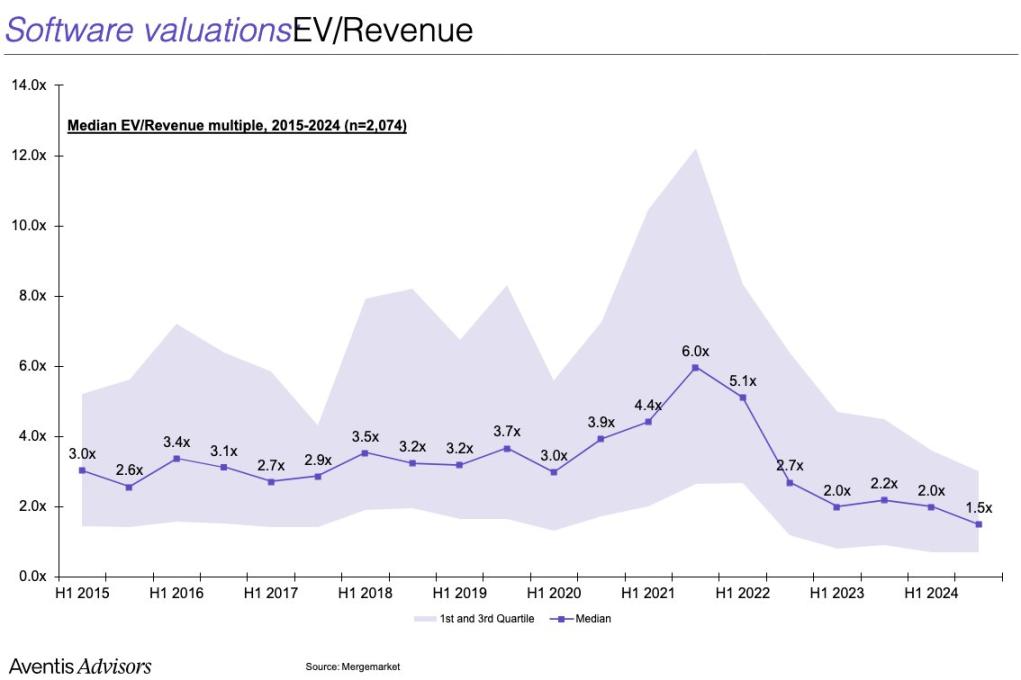

For growth investors who raise funds to bet on disruptive innovation narratives, the reality is: AI asset valuations are generally inflated, and other "growth stories" are difficult to tell with novelty. Once-prominent FAANG stocks are now gradually transforming into mediocre "compounding stocks" focused on maximizing profits. The median price-to-sales ratio (enterprise value/sales) of current software companies has dropped to below 2 times.

As a result, cryptocurrency has returned to the spotlight.

Bitcoin broke through its historical high; the U.S. President "strongly advocated" crypto assets at a press conference; a series of regulatory tailwinds have brought this asset class back to mainstream view for the first time since 2021.

Unlike the previous cycle's Non-Fungible Tokens and Doge, this round's protagonists are digital gold, stablecoins, "tokenization," and payment system reform. Stripe and Robinhood declared that their next phase focus is on crypto business; Coinbase was successfully included in the S&P 500; Circle showed a sufficiently sexy growth narrative to the capital markets, making investors once again ignore valuation multiples and focus on potential stories.

But what does this have to do with ETH?

For crypto natives, the battle of smart contract platforms has long been divided: Solana, Hyperliquid, and countless high-performance new chains and Rollup platforms truly threaten Ethereum's dominance.

We know that Ethereum has not yet truly solved the value capture problem, and we also know that it is facing structural challenges.

But Wall Street is unaware of these. In fact, most Wall Street practitioners know almost nothing about Solana. In terms of familiarity, veteran coins like XRP, LTC, LINK, ADA, and Doge might have more presence in their minds than SOL. After all, these people have almost completely faded from the crypto market in the past few years.

What they know is that ETH is "lindy" - standing the test of time; it has been tested through multiple market fluctuations; for a long time, it has been the main "Beta" asset besides Bitcoin. They see that ETH is one of only two crypto assets with spot ETFs. What they prefer is a "value trap" with relatively cheap valuation and upcoming catalysts.

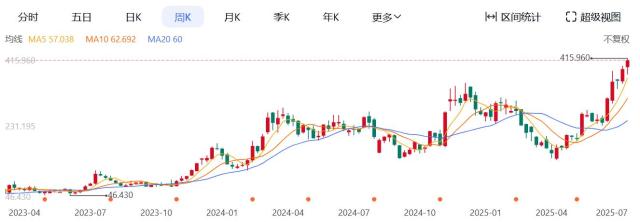

In their eyes, Coinbase, Kraken, and Robinhood have all chosen to build products on Ethereum. With a little due diligence, they can know that Ethereum has the largest on-chain stablecoin pool. They start doing "moon calculations" - and then discover that Bitcoin has set a new high, while Ethereum is still more than 30% away from its 2021 peak.

For them, this "relative undervaluation" is not a risk, but an opportunity. They are more willing to buy an asset that is still low and has a clear target price, rather than chase a coin that is "too late" on the chart.

And they may have already entered. Now, institutional investment compliance restrictions are no longer a big problem. As long as there is sufficient incentive, any fund can seek to allocate crypto assets. Although crypto Twitter (CT) has been swearing for the past year that they would "never touch ETH" again, based on market performance this year, ETH has been outperforming other mainstream assets for over a month.

So far, SOL/ETH has dropped nearly 9% year-to-date; Ethereum's market cap dominance has begun its longest rally since mid-2023 after bottoming in May.

So the question is: If the entire crypto community believes ETH is a "cursed coin," why is it still outperforming?

The answer is: It is attracting new buyers.

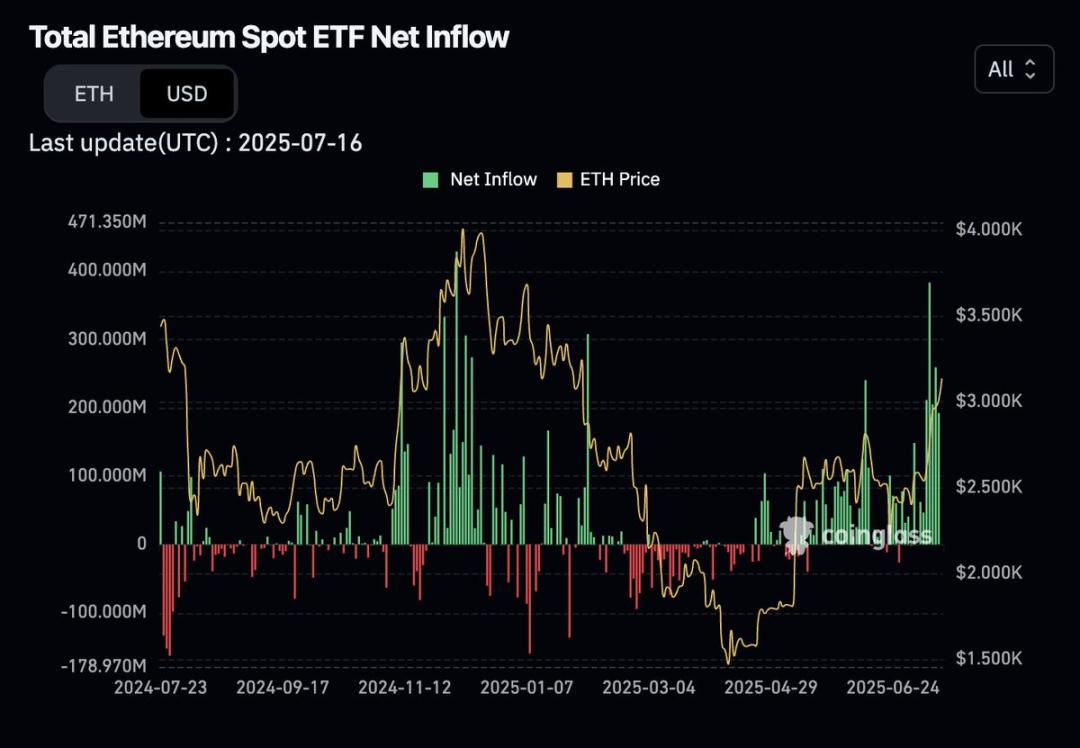

Since March, Ethereum spot ETF net inflows have been in an "up only" mode.

(Data source: Coinglass)

Ethereum "accumulators" stocks mimicking the MicroStrategy model are taking off, injecting structural leverage into the market.

At the same time, some crypto native users may have realized their under-allocation and started moving funds out of BTC and SOL, which have already risen significantly in the past two years.

It needs to be clear that we are not saying the Ethereum ecosystem has solved its problems. Rather, the ETH asset is beginning to gradually "decouple" from the Ethereum network.

External buyers are reshaping the market narrative about ETH, from "decline is certain" to a paradigm shift of "valuation reassessment". Short sellers will eventually be squeezed out, at which point native funds may also join the chase, and ultimately we may usher in a market frenzy centered on ETH, reaching a climactic top at some point.

If this happens, ETH's historical high may not be far away.

Recommended Reading:

With Firm Prices, A Comprehensive Overview of ETH's Four Major "Buying Pressures"